Despite a prevailing sentiment of heightened demand from Asian economies facing acute energy security challenges, global coal prices experienced a notable retreat on Tuesday, March 24, 2026. The benchmark thermal coal price closed at US$139.75 per ton, registering a 0.53% decline. This dip extended a negative trend, with coal prices falling by 4.6% over the preceding two days. This recent downward movement stands in stark contrast to a robust rally just days earlier, from March 19-23, 2026, when prices soared by 8.7%, touching US$146.5 per ton. This previous peak represented the highest level recorded since October 17, 2024, underscoring the extreme volatility currently characterizing the global energy markets. The immediate cause of this recent slump appears to be a broader weakening in the natural gas market, with gas prices plummeting by 3.7% on the same Tuesday. As complementary fuels, the price movements of natural gas and coal often exhibit a strong correlation, particularly in the power generation sector where fuel switching is a common practice. This dynamic overshadowed other geopolitical factors that might otherwise have bolstered coal’s appeal.

Recent Market Volatility and Divergent Trends

The global energy market has been a theatre of significant price swings, reflecting a complex interplay of supply-demand fundamentals, geopolitical tensions, and macroeconomic factors. The recent trajectory of coal prices exemplifies this turbulence. Following a period of relative stability, thermal coal saw a sharp uptick in mid-March, fueled by growing concerns over energy supply disruptions emanating from the Middle East. This rally, however, proved ephemeral, giving way to a two-day decline that erased a substantial portion of the gains.

The immediate trigger for the latest downturn in coal prices was the concurrent fall in natural gas futures. Natural gas, particularly Liquefied Natural Gas (LNG), is a key competitor to thermal coal in many power generation markets, especially in Asia. When gas prices decline, it often makes gas-fired power generation more economically attractive, reducing demand for coal. This "fuel switching" mechanism is a critical driver of short-term coal price movements. Analysts point to factors such as robust European gas storage levels, potentially milder weather forecasts in key consumption regions, or an unexpected increase in LNG supply availability as possible contributors to the gas price drop, which then exerted downward pressure on coal.

Interestingly, this decline in coal prices occurred even as crude oil markets surged. West Texas Intermediate (WTI) and Brent crude benchmarks both saw gains exceeding 5% on the same Tuesday, driven by escalating tensions in the Middle East, particularly around the Strait of Hormuz, and concerns over potential supply disruptions from major oil-producing regions. The divergence highlights the distinct drivers for different energy commodities. While geopolitical instability often impacts all fossil fuels, the immediate price response can vary based on specific supply chains, demand sectors (e.g., transport for oil vs. power generation for coal/gas), and the fungibility of the commodities. The robust demand for oil, tied to global economic activity and geopolitical risk premiums, did not translate into similar support for coal on this particular trading day, suggesting that the immediate fundamentals of the power generation market, especially the gas price, took precedence.

The Interplay of Gas and Coal Markets

The relationship between natural gas and coal prices is foundational to understanding dynamics in the global power sector. Both are primary fuels for electricity generation, and their relative cost heavily influences utility decisions. This phenomenon, known as "fuel switching," allows power plant operators to shift between burning coal and natural gas based on which is more economical, provided their infrastructure allows for it. When natural gas prices are low, utilities may opt for gas over coal dueucing coal demand and, consequently, its price. Conversely, when gas prices spike, coal becomes the preferred, cheaper alternative, boosting its demand and price.

The global LNG market has seen significant fluctuations in recent years. The war in Ukraine, for instance, dramatically reshaped European energy policies, leading to a scramble for LNG and driving up global prices. However, subsequent efforts to secure diverse supplies, build new regasification terminals, and a relatively mild European winter in some years have helped to stabilize, and at times, depress gas prices. In Asia, the spot LNG market is particularly sensitive to supply disruptions, weather patterns, and industrial demand. A sudden increase in LNG cargo availability or a drop in expected demand in key Asian markets can quickly ripple through the market, influencing gas prices and, by extension, coal.

The recent 3.7% fall in gas prices suggests that either supply outstripped demand momentarily, or market sentiment shifted due to factors such as updated weather forecasts indicating less need for heating/cooling, or a reduction in industrial activity. This created a cost advantage for gas-fired power generation, prompting some utilities to reduce their coal consumption, contributing directly to the observed decline in coal prices.

Geopolitical Tensions and Asia’s Energy Security Imperative

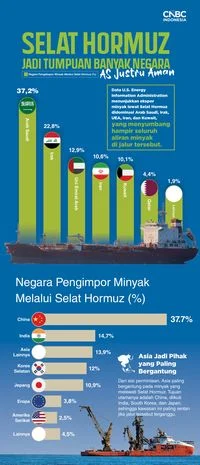

The broader backdrop against which these market movements are playing out is one of heightened geopolitical instability, particularly in the Middle East. The escalating conflict involving Iran and its proxies, coupled with the potential for disruptions in critical maritime chokepoints like the Strait of Hormuz, has sent shockwaves through global energy markets. The Strait of Hormuz, a narrow waterway connecting the Persian Gulf with the Arabian Sea, is arguably the world’s most important oil transit chokepoint. Approximately one-fifth of global oil consumption, and a significant portion of the world’s LNG supply, passes through this strait. Any perceived threat to shipping in this region immediately triggers concerns over supply security, leading to price spikes in crude oil and, indirectly, impacting LNG and other energy commodities.

For Asian nations, which are heavily reliant on imported energy – particularly LNG and oil from the Middle East – these disruptions pose an existential threat. Countries like Japan, South Korea, China, and India are among the largest importers of crude oil and LNG globally, with a substantial portion of these imports transiting the Strait of Hormuz. The vulnerability of these supply lines has forced Asian policymakers to re-evaluate their energy strategies, placing an unprecedented emphasis on energy security and resilience. The "fragility" of Asia’s energy system, as highlighted by the ongoing tensions, has prompted a pragmatic, albeit controversial, pivot back to coal.

Coal, despite its environmental drawbacks, offers several compelling advantages in a crisis: it is widely available, relatively cheaper than imported LNG or oil, and its infrastructure for extraction, transport, and combustion is well-established across many Asian nations. This makes it an immediate and readily deployable "emergency savior" when other, cleaner, or more market-sensitive energy sources become unreliable or prohibitively expensive. This shift reflects a difficult trade-off between urgent energy security needs and long-term climate commitments.

Asia’s Pivot to Coal: National Strategies and Urgent Needs

In the face of these energy vulnerabilities, several Asian economies are making strategic decisions to bolster their coal-fired power generation capacity, even as they pursue ambitious renewable energy targets. This dual approach underscores the complexity of balancing economic growth, energy security, and environmental sustainability.

China, the world’s largest consumer and producer of coal, exemplifies this strategy. Since 2021, China has embarked on a massive program to build new coal-fired power plants, adding record amounts of coal capacity to its grid. This move is primarily driven by a national imperative to enhance energy resilience and avoid blackouts, which have plagued some regions in the past. While China continues to be a global leader in renewable energy deployment, its national policy explicitly supports the continued, and even expanded, use of coal for baseload power generation to ensure grid stability and meet surging industrial and residential demand. The availability of vast domestic coal reserves further reinforces this strategy, reducing reliance on volatile international energy markets.

India, the second-largest consumer and producer of coal, faces similar challenges. With its rapidly growing economy and a population susceptible to extreme summer heatwaves, India anticipates peak electricity demand reaching an unprecedented 270 gigawatts (GW) – nearly double the entire electricity capacity of Spain. To meet this massive demand surge and prevent power outages, India is heavily relying on its extensive domestic coal reserves, estimated to last for approximately three months. The government has directed power generators to ensure full operational readiness of coal-fired plants. Furthermore, in a stark illustration of priorities during a crisis, vital energy imports such as Liquefied Petroleum Gas (LPG) successfully navigating the Strait of Hormuz are likely to be allocated to critical industries like fertilizer production, rather than diverted to power generation, further underscoring the reliance on coal for electricity.

Beyond the two giants, other Asian nations are also adjusting their energy policies:

- South Korea, a highly industrialized nation heavily dependent on energy imports, has reportedly relaxed restrictions on the use of coal-based electricity, signaling a temporary reprioritization of energy security over environmental targets.

- Indonesia, a major coal exporter, has implemented policies to secure domestic supply, such as the Domestic Market Obligation (DMO), to ensure its own power needs are met before exports are considered.

- Vietnam, Thailand, and the Philippines are all reportedly increasing the operational hours and capacity of their existing coal-fired power plants (PLTU) to shore up their electricity grids.

- The Philippines, in particular, has faced such severe energy pressures that it has declared a national energy emergency status, highlighting the acute nature of the crisis in some parts of the region.

The rationale behind this widespread pivot to coal is pragmatic: coal is readily available, its relative cost is lower compared to the volatile prices of imported LNG and oil, and the necessary infrastructure for its use – from mines to power plants and transmission lines – is already largely in place. This makes it the most rational and immediate option for ensuring energy supply stability in times of crisis, despite its significant environmental footprint.

The "Temporary Patch" Dilemma: Short-term Relief vs. Long-term Risks

While coal provides a crucial "temporary patch" for Asia’s immediate energy security woes, experts caution that a prolonged or deepened reliance on it could become a "long-term trap." The immediate benefits of utilizing coal are undeniable: it stabilizes electricity supply, mitigates the economic shock of soaring import prices for other fuels, and provides a buffer against geopolitical disruptions. For nations facing potential blackouts or economic slowdowns due to energy shortages, these short-term gains are paramount.

However, the implications of a sustained return to coal are far-reaching and detrimental:

- Environmental Impact: Coal is the most carbon-intensive fossil fuel, meaning its combustion releases the largest amount of greenhouse gases per unit of energy produced. Increased coal burning directly undermines global efforts to combat climate change, making it harder to meet targets set under the Paris Agreement and other international accords. It also contributes significantly to air pollution, leading to severe public health issues in urban centers across Asia.

- Climate Goals: Many Asian nations have committed to decarbonization pathways and net-zero targets. A renewed reliance on coal creates a significant obstacle to achieving these goals, potentially leading to international criticism and economic repercussions (e.g., carbon border adjustments).

- Stranded Assets: Investing in new coal-fired power plants or extending the lifespan of existing ones carries the risk of creating "stranded assets." As the world inevitably transitions towards cleaner energy, these assets may become economically unviable or politically unacceptable before the end of their operational life, resulting in significant financial losses.

- Economic Diversification: Over-reliance on any single energy source, even a domestically abundant one, can hinder the diversification of energy portfolios and delay investment in truly sustainable alternatives like renewables, nuclear, and advanced energy storage solutions.

- Reputational Costs: Nations heavily investing in coal may face reputational damage on the global stage, impacting their ability to attract green finance or participate in international climate initiatives.

Analysts suggest that while the current circumstances necessitate a pragmatic approach, policymakers must view coal as a stopgap measure. The real challenge lies in accelerating the transition to a more diversified and sustainable energy mix that can withstand future geopolitical shocks without resorting to environmentally damaging solutions. The ongoing crisis should serve as a powerful impetus for increased investment in renewable energy sources, grid modernization, regional energy cooperation, and energy efficiency measures, rather than a justification for long-term coal dependency.

Expert Perspectives and Future Outlook

Energy experts and international organizations are closely monitoring Asia’s energy choices. Many acknowledge the difficult position Asian nations find themselves in, caught between immediate energy security needs and long-term climate commitments. However, there is a broad consensus that while coal might offer a temporary lifeline, it is not a sustainable long-term solution.

"The current geopolitical landscape has exposed the raw nerves of energy insecurity, particularly for import-dependent Asia," commented a senior energy analyst from a Singapore-based consultancy. "Coal provides a quick fix, but it’s like using a band-aid for a deep wound. The underlying issue is the lack of diversified, resilient, and domestically controlled clean energy sources. This crisis should be a wake-up call to accelerate, not decelerate, the green transition."

Looking ahead, the global energy market is likely to remain volatile. The interplay between geopolitical events, economic growth, and the pace of energy transition will continue to shape commodity prices. For Asia, the immediate future will involve a delicate balancing act: ensuring sufficient energy supply to power economic activity and protect populations, while simultaneously working towards a cleaner, more sustainable energy future. The decisions made in the coming months and years will have profound implications not only for the region but also for the global fight against climate change. The current retreat in coal prices, despite the strong underlying demand drivers from Asia, serves as a stark reminder of the complex and often contradictory forces at play in today’s energy landscape.

The reliance on coal, a relic of the industrial age, underscores the profound challenges inherent in transitioning to a low-carbon economy, especially when confronted with the immediate and pressing demands of national energy security in an increasingly unstable world. The path forward for Asian economies will require innovative policy-making, substantial investment in new technologies, and a concerted effort to build truly resilient and sustainable energy systems that can withstand both market fluctuations and geopolitical shocks.